First Quarter 2020

“We will remain vigilant in pursuing opportunities to improve the risk/return profile of the portfolio.”

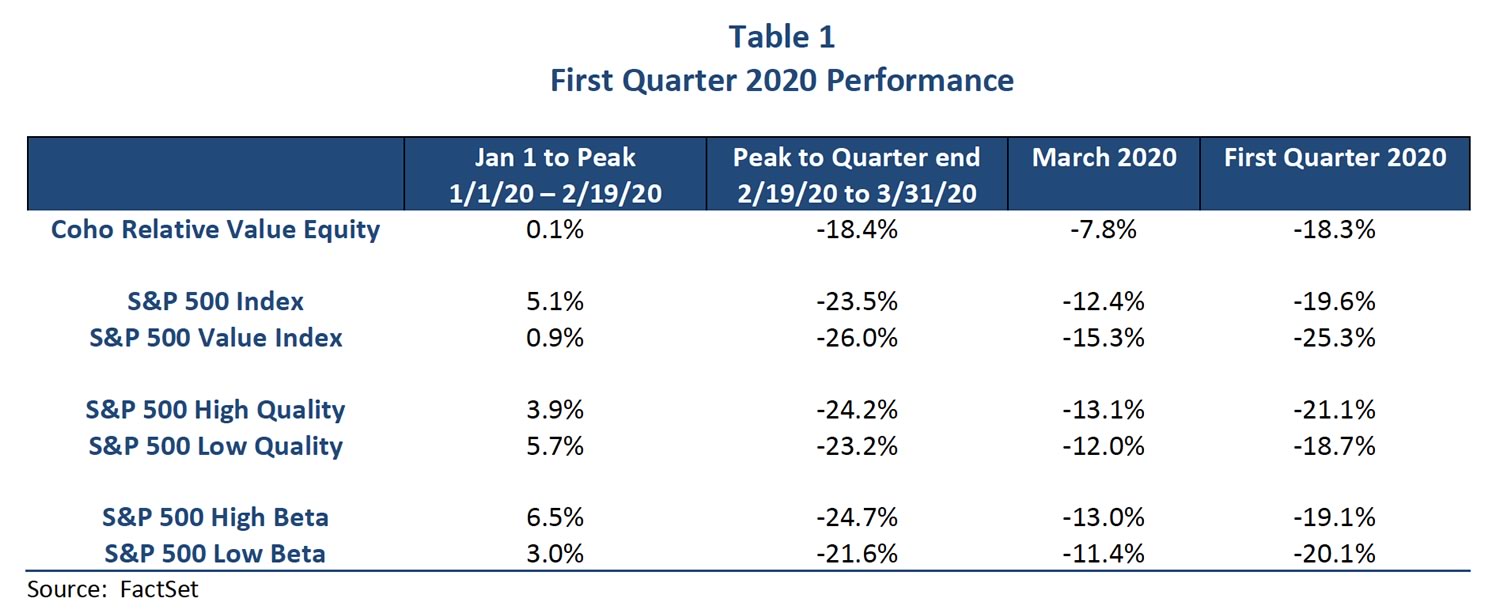

The volatility in March has stunned all investors, both new and old. At one point during the month, the S&P 500 Index was down over 29%. When the month ended, the S&P 500 Index had declined 12.4% and the Coho Relative Value Equity portfolio was down 7.8%, capturing just under 64% of the fall. The first quarter of this year was bifurcated into two distinct periods.

The first, from the onset of the year to the peak on February 19th, saw the S&P 500 Index gain 5.1% compared to only slightly positive returns for Coho. The second, from the peak to the end of the quarter, the S&P 500 Index declined 23.5% and Coho declined 18.4%. During this period there were 34 trading days. Included in these were eight days with declines of more than 3%, eight days with gains of more than 3%, a 9.5% decline on March 12th., and two up 9%+ days on March 13th and March 24th. March was the most volatile month in the history of the New York Stock Exchange.

The root cause of this schizophrenic trading was the sudden outbreak of the global pandemic now known as the coronavirus or COVID-19. The impact on the U.S. economy has been startling, as we started the year with record low unemployment, high consumer confidence and rising wages. Now we are confronted with the closure of all non-essential businesses, unemployment spiking, consumer confidence falling, and the stock market in bear market territory.

The three most pressing questions might be: one, how did Coho perform during this period; two, what actions did you take to reposition the portfolio; and three and perhaps the most important one, where will the market go from here.

Table 1 breaks the first quarter performance into four periods: 1) the start of the year to the peak on February 19th, 2) the peak to the end of the quarter, 3) the month of March, and 4) the full first quarter 2020. Looking at factors such as quality and volatility, one can see that there was very little separation between these during this quarter. Perhaps much of that was due to the sheer suddenness and magnitude of the correction. and the fact that it occurred in the absence of any material earnings releases. There were many down days during this period as every sector got hit indiscriminately (a market “flush” as we have often described it). Another plausible explanation could be that the impact of the virus cut across so many disparate companies and sectors as so much of the economy was effectively shut down. Finally, the market is working through a massive economic disruption with very little actual observable data from individual corporations. Many, if not most, companies have pulled their guidance for the upcoming quarter and even the entire year given all the uncertainty as to how this virus plays out. Whatever the reason or combination of reasons, the differentiation in quality and volatility that we historically have observed in previous corrections was not evident in this quarter. We will get much more actual data and projections as companies report their first quarter earnings and relate the impact the virus and the shutdown has had on their businesses. We remain confident that companies which can show strong relative earnings stability will attract investor interest and that our companies should have this type of durability.

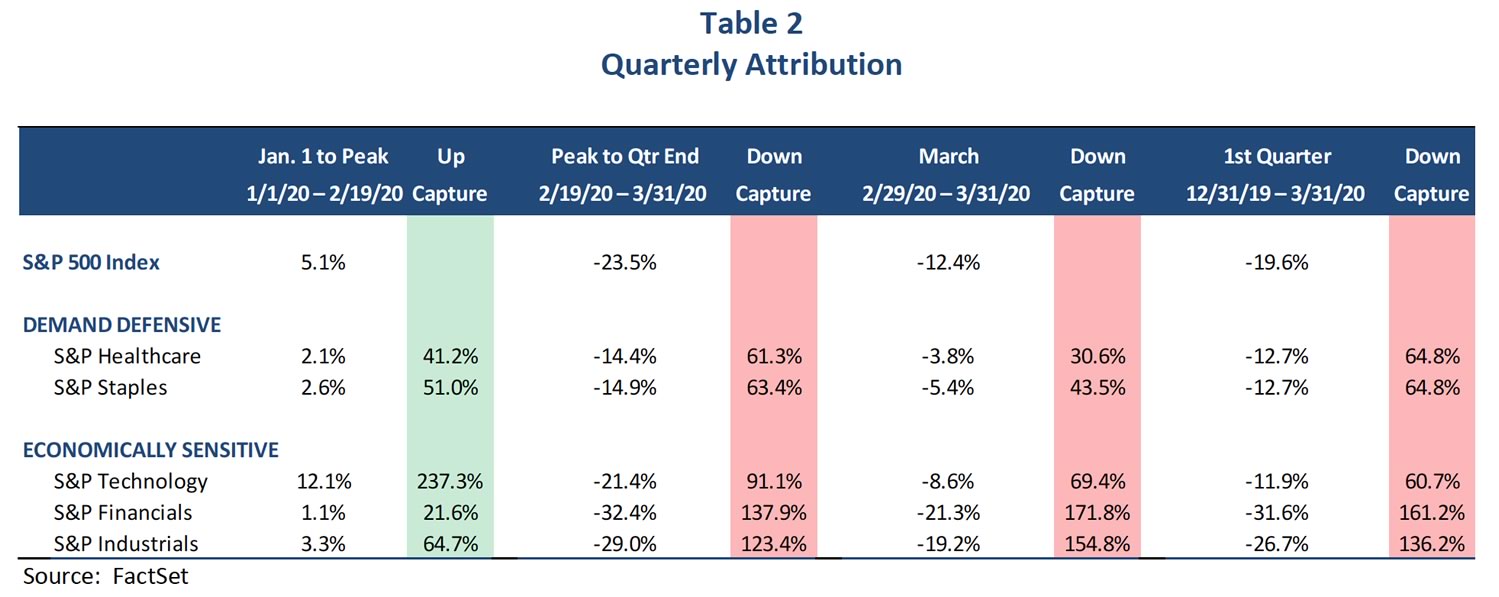

Coho did not participate as fully as we would have liked during the initial rising period, but we were able to provide some reasonable downside protection during the sell-off. Putting it all together, we were able to slightly outperform the S&P 500 Index for the quarter. Still, this is a far cry from what we would want with regards to preservation of capital during a correction. Table 2 takes the same periods as seen in Table 1 and shows how our two major demand defensive sectors as well as some of the major economically sensitive sectors performed.

Market history has clearly shown that during cyclical corrections the Demand Defensive sectors, such as Consumer Staples and Health Care typically outperform because their earnings stability tends to be much stronger than the more Economically Sensitive sectors where the cycle has a much greater impact. This pattern broadly held during this downturn. While our relative returns benefited greatly from our overweights in the defensive sectors over the quarter, some of that benefit was materially muted in the S&P 500 Index by one cyclical sector in particular, Information Technology.

We recognize that certain of these Technology companies such as Microsoft and Adobe, for example, have evolved their business models to reduce some of their historical cyclicality by becoming more subscription based. Subsequently, however, the market has rewarded them with valuations that we feel more than compensate for their lower cyclicality, so while they are in our investable universe, they have remained outside of our valuation discipline. But Technology now represents more than 24% of the S&P 500 Index and is nearly double the next largest sector, Health Care, at about 14%. As such, the S&P 500 Index’s return can be greatly influenced by how the Technology sector performs (much less so for the value index where the weight is closer to 7%). For the quarter, Technology did materially outperform the benchmark in a down period, but the vast majority of this alpha came during the rising period from the beginning of the year to the market’s peak in February. Technology picked up right where it left off in 2019 and was by far the most dominant positive sector from the start of the year to the market peak. However, during the correction that followed through the end of the quarter, Technology performed essentially in line with the index. While we continue to monitor the evolution of the industry, this performance does not suggest to us that Technology has established itself as a “new defensive” sector. Nevertheless, because of its huge start to the year, it showed impressive relative returns point-to-point for the full quarter. It will be interesting to watch as the sector balances the very near-term benefits from extra demand driven by so many people working from home, versus the likely cyclical downward pressures on tech spend by the corporate sector in a slower economy. Coho remains underweight Technology and as such our lower allocation to this sector negatively impacted our returns by approximately 270bps in aggregate vs. the S&P 500 Index, but had very little impact on our relative returns vs. the value index which holds much less weight in that sector.

During this period of unprecedented uncertainty and market volatility, we focused primarily on two issues: one, are there companies currently in the portfolio that could be fundamentally and severely damaged by the current environment and; two, are there companies in or outside of the portfolio that are being priced as if they will be fundamentally damaged by the current environment but in reality have the ability to withstand and prosper longer term. Basically, are there companies that we own that now risk moving from high quality to low quality, and conversely, are there high-quality franchises caught up in the market maelstrom that will be fine longer term?

As a result, we took decisive actions during the volatility in March by eliminating two of our Energy holdings, initiating new positions in Coca-Cola and Sysco, and adding to our existing positions in Chevron, Lowes, Ross Stores, and Unilever. We firmly believe that these trades increased the quality of the portfolio and enhanced our ability to deliver our pattern of returns focused on downside protection and upside participation. Selling both Occidental Petroleum and Royal Dutch resulted from position paper violations. The recent spat between Russia and Saudi Arabia has cratered crude prices. This is the first time in our memory where a demand issue (the shutdown due to the virus) was exacerbated by a deliberate and massive increase in supply. Our work indicates that if oil were to remain near the current $20 level, neither of these companies would have been able to cover their dividend, and we were not surprised by Occidental’s Board decision to greatly reduce theirs so quickly. We were able to sell our position prior to this action, which was some modest consolation. We used some of those Energy Coho Partners, Ltd. Portfolio Commentary: March 31, 2020 Page 4 proceeds to add to our Chevron position. Chevron continues to have a great deal of financial flexibility and the company is a low-cost producer, so they should be able to weather this storm and come out stronger on the back end.

The new positions in Coca-Cola and Sysco were both opportunistic and valuation driven. In the case of Coca-Cola, the stock had declined from a recent high of $59 to $38 on March 23rd when we initiated our position. At $38, Coke had an attractive risk/return, the price earnings multiple was down to 17.2x on 2021 earnings, and its dividend yield was 4.3%. The company’s global position in both carbonated and still beverages is second-to-none and as per capita income around the globe continues to rise, there will be an increasing demand for Coke’s products.

Sysco, which is the largest domestic foodservice company, was down from a recent peak of $73 on March 3rd to less than $30 on March 16th when we started this position. Sysco’s customers are “away from home diners”, meaning they service restaurants, educational institutions, hospitals and other similar type establishments. Many of these businesses are now closed so there will clearly be a near-term impact on the company’s earnings, but we strongly believe that as this pandemic passes, the customers will return, and Sysco will remain the provider of choice for them. In the meantime, Sysco is re-purposing its vast supply chain to help restock grocery stores which need assistance serving their current spike in demand. We believe we were able to buy a world-class company trading at a highly attractive valuation on realistically reduced expectations, yielding more than 6% with a solid balance sheet and the liquidity to withstand the near-term severe disruptions.

Late in the month, we added to Lowe’s, which had fallen from about $120 in late February to less than $90 at time of purchase. Lowe’s is deemed an essential business so all its stores will remain open and available to service its customers. The operating environment prior to the COVID-19 impact was quite favorable, with rising home values, historically low interest rates, and strong consumer confidence. Unless this pandemic lasts far longer than we expect, the change in value created an excellent buying opportunity.

We added to our position in Ross Stores after the stock had dropped from $125 in late February to $98 in early March. Ross is an off-priced retailer, basically liquidating excess inventories and overruns from other retailers and manufacturers. The quality and selection of off-priced goods for Ross is going to be unprecedented when the stores are able to open again. Even if the economic recovery is halting, the average price point at Ross is under $10, so historically their stores continue to do well in difficult economic environments.

Finally, Unilever also came under pressure as concerns about emerging markets increased. Unilever is well positioned in all the major emerging markets, and this pandemic could increase demand for its staple personal hygiene products.

Some might argue that the “cure” of the economic shutdown is worse than the “disease” itself, as so many people now find themselves out of work and close to economic ruin. In response, the coordinated actions of our Government are unprecedented in their size and scope. Clearly the goal is to get ahead of the virus curve so that the U.S. and other countries can return to a more normal work environment. The timing of this remains uncertain, but it will happen, and when it does, people will likely start to return to Coho Partners, Ltd. Portfolio Commentary: March 31, 2020 Page 5 their favorite places, employees will be rehired, and life will return to a more normal pace. The trajectory of the recovery will be gradual. The second quarter GDP estimates are still coming in, but it seems reasonable to expect our GDP to be down double digits, which we hope would be the worst quarter for this year and that the second half would show some meaningful improvement. One fact seems clear and that is that the sooner the virus is contained, the sooner our country and others can return to better economic conditions and that should portend higher stock prices.

The entire world would like to see the virus contained sooner rather than later; however, if COVID-19 persists for longer than anticipated, we believe the Coho portfolio is well positioned. At the end of the quarter, approximately 60% of the portfolio’s weight was in “demand defensive” companies, which compares to 32% for the S&P 500. As such, the portfolio should have a more stable earnings pattern than their more cyclical counterparts. ConAgra, one of our Consumer Staples holdings with a strong position in frozen food and snacks, just reported earnings for its fiscal third quarter ending in February. Management gave an upbeat forecast for the fiscal fourth quarter and this momentum could easily continue into the next fiscal year. While ConAgra may benefit more than most from the increase in at-home food consumption, there are a number of other portfolio benefactors such as Dollar General, Kroger, J.M. Smucker and Unilever.

The pundits are predicting April as a critical month to “ flatten the curve” on this virus, and we hope this proves accurate. In the meantime, volatility will remain elevated and we will remain vigilant in pursuing opportunities to improve the risk/return profile of the portfolio. We wish everyone good health and to stay safe.

If you have questions or concerns about our outlook or the portfolio’s positioning, please do not hesitate to call us. We look forward to updating you on the progress of the portfolio as the year progresses.

Sincerely,

Coho Partners’ Research Team

The views, opinions and content presented are for informational purposes only. They are not intended to reflect a current or past recommendation; investment, legal, tax, or accounting advice of any kind; or a solicitation of an offer to buy or sell any securities or investment services. Nothing presented should be considered to be an offer to provide any Coho product or service in any jurisdiction that would be unlawful under the securities laws of that jurisdiction. Past performance is not indicative of future results.